FX Markup: The EOR Fee No One Discloses on Sales Calls

Of the seven cost layers in a typical EOR contract, FX markup is the most opaque — and on a 20-employee team, it costs more per year than the negotiated service-fee discount. Provider benchmarks from Deel (0%) to legacy providers (5%+), plus the contract redline that locks the spread.

.png)

FX markup is the EOR fee that doesn't appear on any quote

Of the seven cost layers in a typical EOR contract, FX markup is the most opaque and the least frequently discussed. It does not appear as a line item on quotes. It does not come up on demo calls unless the buyer asks directly. It is not included in standard pricing comparisons. And yet, on a typical 20-employee international contract, it costs more per year than the negotiated discount on the headline service fee.

The mechanic is simple. You pay your EOR in USD, EUR, or GBP. Your employees are paid in MXN, BRL, INR, or any other local currency. The conversion between those two currencies happens somewhere in the cost stack, and the EOR pockets the spread between the rate they get on the wholesale market and the rate they charge you. That spread — typically 1–3%, but ranging from 0% to 5%+ across the industry — is the FX markup. On $100,000/month of local-currency payroll, a 3% spread is $36,000 per year. A 1% spread is $12,000. The difference is $24,000 per year, invisible in the headline numbers.

Most buyers never think to ask, because FX is not framed as a fee. The quote does not call it FX markup. The contract typically does not specify a rate methodology. The invoice shows a billing-currency total without the conversion math. And the provider's sales team is trained not to volunteer information that does not get asked for. This post explains how FX markup works mechanically, why it stays hidden, what it actually costs, where it hides in your quote, and how to negotiate it down or out before signing. Pair with the quote decoder and the negotiation playbook for the full procurement workflow.

How EOR FX markup actually works

The mechanic in three steps. First, the EOR receives your payment in billing currency (USD, EUR, GBP) covering gross salaries, employer statutory, benefits, and service fee — denominated in your currency even though the underlying payments will be made in local currencies. Second, the EOR converts the local-currency cost into your billing currency at an FX rate it sets at its own discretion, within the contractual language. Third, when payment is received, the EOR converts back to local currency through its bank or treasury operations, capturing the spread between the wholesale rate it gets and the rate it charged you.

The wholesale rate the EOR receives sits very close to the mid-market rate — the rate at which banks trade currencies with each other, which Bloomberg, XE, OFX, and Reuters publish in real time. That is the floor. The rate the EOR charges you sits above that floor by some spread, and the spread is the markup. The flow, stage by stage:

Mid-market rate — the interbank rate published by XE, Bloomberg, and OFX. This is what banks pay each other on the wholesale market.

EOR wholesale rate — mid-market + 0–30 basis points. This is what the EOR's treasury actually receives when it converts.

EOR retail rate — mid-market + the disclosed spread (the markup). This is the rate you are billed at on your invoice.

FX margin — retail rate minus wholesale rate. This is the EOR's FX revenue on every transaction.

The spread is the provider's FX margin. It ranges from 0% (Deel publishes a mid-market policy) to 5%+ (some legacy providers). Most providers sit in the 1.5–3% range. The number is rarely stated in plain language; it is typically embedded in contract clauses vague enough to permit discretion — "prevailing market rate," "bank rate," "conversion at the applicable exchange rate" — rather than a specific methodology.

Why providers do not disclose FX markup

Five reasons FX stays in the background of every EOR sales conversation.

The margin is large enough to matter. For a provider running $10M+ in monthly cross-currency payroll volume, a 2% spread is $200,000+ per month in pure margin. Disclosing the rate methodology and committing to a specific spread surrenders meaningful margin to negotiation. The incentive to keep it discretionary is real.

The discretion is operational, not just commercial. A provider that quotes a fixed spread loses flexibility to manage treasury risk, hedging costs, and operational overhead — especially in volatile-currency markets. Some of the discretionary language is genuine operational flexibility rather than pure margin grab. The buyer cannot easily tell which.

Comparison is harder when FX is bundled. If providers disclosed FX spreads explicitly, buyers could compare them directly the way they compare headline service fees. As long as FX is folded into the billing-currency total, apples-to-apples comparison requires the buyer to do manual reverse-engineering most buyers will not do.

Buyers rarely ask. Procurement teams are trained to negotiate on the headline service fee. Few are trained to ask about FX, fewer to demand specific numbers in writing, and fewer still to insist on contract language that locks the spread methodology, the timing, and the per-currency uniformity.

The fee is not easily auditable after the fact. Without the rate methodology in the contract, the invoice arrives in billing currency and the buyer cannot reconstruct what rate was applied. Even with the methodology disclosed, auditing each invoice against historical FX data takes work, and most buyers do not.

The combined effect is a fee that almost everyone pays and almost no one negotiates.

What FX markup actually costs — the math

Concrete numbers, based on a 20-employee international team with average gross salary of $5,000/month per employee. That is $100,000/month in local-currency payroll, or $1.2M annually. The FX cost at different spread levels:

0% spread (Deel's mid-market policy) — $0/month. $0/year. $0 over three years.

1% spread (best-in-market outside Deel) — $1,000/month. $12,000/year. $36,000 over three years.

2% spread (typical major provider) — $2,000/month. $24,000/year. $72,000 over three years.

3% spread (typical mid-tier provider) — $3,000/month. $36,000/year. $108,000 over three years.

5% spread (legacy / regional provider) — $5,000/month. $60,000/year. $180,000 over three years.

For context, the negotiated discount on headline service fee for a 20-employee deal is typically $50–$100 per employee per month — $12,000–$24,000 per year. A move from a 3% FX spread to a 1% spread on the same contract is $24,000/year saved. That is equal to or larger than the headline-fee discount almost every procurement team focuses on.

The cost scales linearly with volume. At 50 employees, a 3% spread costs $90,000/year. At 100 employees, $180,000/year. At enterprise scale, FX margin can exceed the entire EOR service-fee revenue on the same contract. The procurement priority should shift accordingly: at higher volumes, FX is the most important variable in the cost stack, not the headline fee.

Provider FX benchmarks in 2026

Based on Compareor's analysis of 1,200+ EOR quotes and post-signing invoice data through Q1 2026, the FX spread by provider:

Deel — Published policy: mid-market rate, 0% spread. Actual disclosed spread in Q1 2026: 0%.

Remote — Published policy: mid-market + 0.5–1.5%. Actual: ~1.2% average.

Native Teams — Published policy: mid-market + 0–1%. Actual: ~0.8% average.

Rippling EOR — Published policy: mid-market + 1%. Actual: ~1.0% measured.

Boundless — Published policy: mid-market + 1%. Actual: ~1.0% disclosed.

Oyster — Published policy: mid-market + 1.5%. Actual: ~1.5% average.

Multiplier — Published policy: "bank rate" (vague). Actual: ~2.2% disclosed, ~2.8% measured.

Papaya Global — Published policy: "bank rate plus margin." Actual: ~2.5% average.

Velocity Global — Published policy: "prevailing market rate." Actual: ~2.5–3% disclosed.

Atlas (LATAM focus) — Published policy: discretionary. Actual: ~2.5–3.5% measured.

Legacy / regional providers — Published policy: discretionary, often opaque. Actual: 3–5%+.

The 2024-to-2026 trend has been compression. Average disclosed FX spread across the market was 2.7% in Q1 2024 and 1.8% in Q1 2026 — a 33% reduction in two years, largely driven by Deel's mid-market policy pulling the rest of the market toward disclosure. The compression is asymmetric: top-tier providers have moved meaningfully, mid-tier providers have moved modestly, and legacy providers have barely moved.

Where FX markup hides in your quote

Five places to look in a typical EOR quote.

The billing-currency total without a local-currency reference. If the quote shows $5,500/month per employee without the underlying local-currency breakdown, the FX is already baked in and invisible. Always demand the local-currency version of the quote alongside the billing-currency version. The local-currency number is the audit anchor.

The rate methodology language in the contract. Search for FX, currency conversion, exchange rate, or applicable rate. If you find phrases like prevailing market rate, bank rate, rate determined by Service Provider, or current exchange rate without a specific methodology, the discretion is locked in and you have no audit path.

The timing of conversion. Some providers convert at invoice issue. Others convert at payment receipt. Others use a monthly average. Each timing has different implications, and the provider chooses the one most favourable to them on average. The contract should specify the conversion date — ideally last business day of the payroll month or a similarly fixed reference.

Per-currency variation. Some providers charge different spreads for different currencies — small spread on EUR/USD/GBP, larger spread on volatile currencies (ARS, TRY, NGN). A flat-spread commitment averages this out; per-currency disclosure exposes the variation. Demand one or the other.

The monthly invoice format. Once running, monthly invoices should show the local-currency cost, the FX rate applied, and the billing-currency total — all three on the same line. If your invoice only shows the billing-currency total, you cannot audit the FX rate retroactively. This invoice format is itself a signal about provider transparency.

The hidden FX levers most buyers miss

Beyond the headline spread number, four mechanisms providers use to capture additional margin even after a spread number is disclosed.

Conversion timing arbitrage. If the contract says conversion at invoice issue date, the provider can choose when to issue the invoice within a window — and the choice will favour them when currencies are moving in a predictable direction. Better contract language: conversion at mid-market rate on the last business day of the payroll month — a fixed date with no discretion.

Per-currency spread blending. A provider that quotes 1.5% FX spread in aggregate might charge 1% on stable currencies and 3% on volatile ones. The blended number sounds reasonable; the per-currency reality is worse. Demand per-currency disclosure or a flat-cap commitment that applies regardless of currency.

Monthly average gaming. Some providers convert at monthly average rate, which sounds neutral but allows the provider to select the most favourable monthly average across daily readings. Better contract language: spot rate on a specific date, or the daily rate on the payment date — both auditable against published sources.

The float interest spread. Many EORs hold a payroll float (1–2 months of expected payroll, deposited upfront). The float sits in the provider's account in your billing currency, earning interest, sometimes for the entire contract term. The interest is implicit FX-adjacent margin. Negotiate either the float waiver or an interest-pass-through clause.

How to negotiate FX in the contract — a 4-step playbook

Step 1: Ask for the number on the demo call. Direct quote: What is your FX spread over the mid-market rate, and will you commit to that number in our contract? Document the answer in writing immediately after the call. If the rep cannot commit a number, that is the answer to the original question.

Step 2: Get the specific language in the contract. Insert: Currency conversion at the mid-market rate as published by XE.com on the last business day of the payroll month, plus a maximum spread of 150 basis points, applied uniformly across all currencies. This locks the methodology, the timing, the spread, and the per-currency uniformity all at once. A 100–150 bps cap is reasonable; anything higher should be justified specifically.

Step 3: Require invoice transparency. The contract should specify the invoice format: local-currency cost, FX rate applied, billing-currency total — all on each line, for every employee, every month. This makes FX auditable invoice-by-invoice and creates accountability after signing.

Step 4: Add an audit right. Insert: Provider will, upon Customer's request, provide the documented FX rate used for each invoice along with corroborating evidence (e.g., screenshot or API record of the XE rate on the relevant date). This is a low-cost commitment that providers should accept without resistance, and it establishes verification capability for the entire contract term.

When FX is your biggest contract risk

Three scenarios where FX dominates the procurement decision.

Volatile-currency markets. Argentina, Turkey, Egypt, Nigeria, Lebanon, parts of Africa, and occasionally Brazil or India in stress periods. In these markets, FX moves 10–30% annually, sometimes in single months. A 2–3% spread is multiplied by the volatility, and the provider absorbs volatility risk by holding wider buffers — which becomes embedded margin. Push hard for spread transparency in these markets, and consider whether your payroll currency arrangement (USD-pegged contracts versus pure local-currency) actually fits the operational reality.

High-volume contracts. At 50+ employees, FX impact scales linearly while the headline service fee discount tapers off. A 100-employee contract with 3% spread costs $180,000/year in FX alone. The negotiating priority should shift from headline fee to FX spread at this scale, because the marginal dollars are bigger.

Multi-currency contracts. If your team spans 10+ countries, you are running 10+ FX exposures simultaneously — different currencies, different volatilities, different spreads if the provider does per-currency pricing. The complexity rewards a flat-spread commitment that applies uniformly across all currencies in scope, rather than provider-set per-currency rates that arbitrage your country mix.

How Compareor advisors handle FX in your evaluation

Standalone, FX is a hard topic to negotiate. The mechanics are technical, the contract language is dense, the providers are not eager to disclose, and most buyers do not have a benchmark to anchor against. A Compareor advisor changes this in three ways.

The benchmark. The advisor knows what each provider's typical FX spread looks like across the industry (per the table above) and brings the data into the negotiation. We are seeing 1.2% from Provider X on similar deals — your 2.5% quote needs to come down or we need to understand why. Anchoring against measured spread, not provider claim, materially shifts the conversation.

The contract language. The advisor brings the specific contract redline that locks the FX methodology, timing, spread cap, and audit right. The redline is provider-vetted — has been accepted by similar providers in similar deals — so resistance is minimised and the negotiation focuses on the number rather than the structure.

The per-currency analysis. For multi-country contracts, the advisor analyses the actual FX exposure across your country mix and identifies whether a flat-spread structure or a per-currency commitment is optimal for your situation. This is the work most procurement teams do not have time to do on their own.

The service is free to buyers — Compareor is compensated by the provider on closing, not by you — and the FX work fits within the broader procurement workflow described in the negotiation playbook, the quote decoder, and the contract red flags guide. Request a Compareor advisor before signing.

Frequently asked questions

What is a fair FX spread for an EOR contract in 2026?

Anything at or below 1.5% (150 basis points) over mid-market is fair in the current market. Below 1% is excellent. Between 1.5–2.5% is the industry average and warrants negotiation. Above 2.5% is above market and should be challenged with benchmark data. Above 4% is structurally problematic — consider a different provider.

Why does Deel offer 0% FX spread?

Deel introduced its mid-market policy in 2022 as a competitive differentiator and recovers margin through its headline service fee and benefits structure rather than through FX. Whether the overall cost is lower depends on the rest of the contract — Deel's headline fee is typically at the high end of the market — but the FX transparency is genuine and the methodology is auditable.

How do I verify the FX rate after the fact?

If your contract specifies the methodology (e.g., XE mid-market rate on the last business day of the month), you can cross-check each invoice against historical XE data, which is publicly available. For audit, request the rate evidence from the provider — a low-cost commitment they should provide on request.

What is the difference between mid-market rate and bank rate?

Mid-market rate is the interbank rate at which banks trade currencies with each other — it is the wholesale floor, and what XE, Bloomberg, and OFX publish. Bank rate is the retail rate banks charge customers, which sits 1–3% above mid-market depending on the bank and the currency. Bank rate in EOR contracts is a vague term that typically means whatever the provider's bank gives us, plus our margin.

Should I pay my EOR in local currency instead of USD/EUR/GBP?

Sometimes. If you have natural local-currency revenue (a sales office in the same country), paying in local currency eliminates the FX conversion entirely on that pair. Most companies do not have this and the operational complexity is not worth it for low volumes. For high-volume single-country contracts, it is worth modelling.

Is FX markup negotiable for small contracts?

Yes, but to a smaller degree. Below 5 employees, you are unlikely to get below 1.5–2% spread from most providers. Between 5–15 employees, 1.5% is achievable. Above 15 employees, 1% or lower is realistic, and at 50+ employees, 0–0.5% is achievable with the right provider.

What happens to FX exposure during high currency volatility?

In volatile-currency markets, provider behaviour varies. Some absorb the volatility within the agreed spread (preferred from a buyer perspective). Others invoke material change clauses to re-quote when the currency moves more than a threshold (problematic — read the red flags guide for how to define material). The contract language matters more in volatile markets than in stable ones.

Bottom line

FX markup is the single most opaque cost line in a typical EOR contract and the cost layer most consistently underestimated by buyers. On a 20-employee team, the difference between a well-negotiated FX spread and a default-quoted one is $24,000–$36,000/year. On a 100-employee team, the difference is $120,000–$180,000/year. On most contracts, that exceeds the headline-fee discount the procurement team focused on.

Three principles separate buyers who manage FX well from buyers who pay default rates. First, ask for the number on the demo call and demand it in writing. Vague language preserves the provider's discretion; specific language preserves yours. Second, get the methodology, the timing, the cap, and the per-currency uniformity all locked into the contract — a single redline does it. Third, require monthly invoice transparency so the cost is auditable in real time, not theoretical after signing.

If you want help locking down FX in your specific contract, a Compareor advisor brings the benchmark data, the provider-vetted redline, and the per-currency analysis for your country mix — all on a call, all free, all before you sign. The benchmark is free. The redline is free. The only cost is signing a contract with the default FX clause and discovering, several invoices later, what the spread actually was.

Get your shortlist

Takes ~3 minutes. No account needed.

June 3, 2026

6 min read

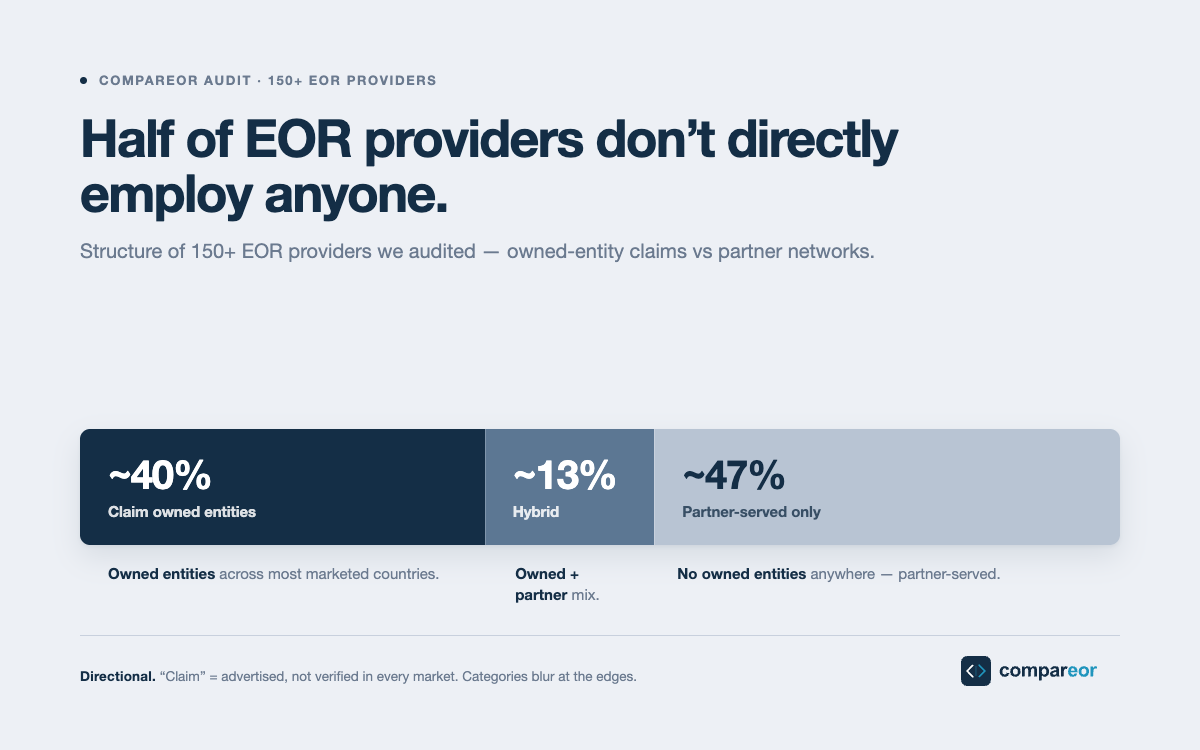

I checked the structure of 150+ EOR providers. Here's how many actually own their entities.

About 40% of EOR providers I audited claim and substantiate owned entities across most of their marketed countries. About 12 to 15% run an honest hybrid. About 45 to 50% are partner-served only, with no owned entities anywhere. The numbers, the methodology, the one honest caveat, and what they mean for buyers.

June 3, 2026

6 min read

Every EOR contract has an expiration date

The EOR model has a built-in expiration date, somewhere between 15 and 20 employees in one country. Past that threshold, the EOR stops being the cheapest option and starts being a tax on growth. Most companies miss it for a year or more, because the contract doesn't mention it and nobody inside is responsible for noticing.

May 25, 2026

5 min read

Why "150+ countries" is the most misleading number in global employment

Every EOR homepage leads with a country count, and after auditing 150+ providers it's the number most likely to lead you to the wrong choice. Coverage comes in three forms, and depth in your countries matters more than breadth across 185 of them.

Stay Updated on Global Hiring

Get weekly insights on EOR trends, compliance updates, and cost-saving strategies

Find a better EOR — without risk

Compare EOR providers to gain insights on cost, coverage, and contract flexibility, ensuring compliance and payroll continuity.

.png)

.png)