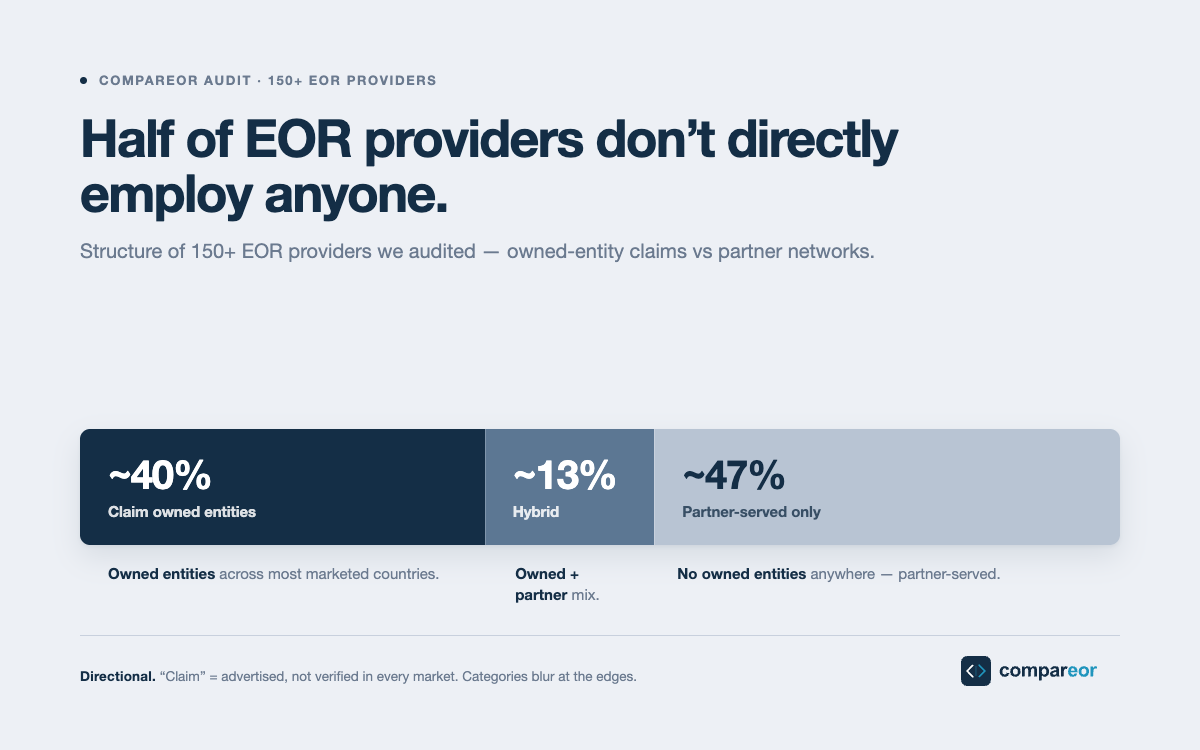

I checked the structure of 150+ EOR providers. Here's how many actually own their entities.

About 40% of EOR providers I audited claim and substantiate owned entities across most of their marketed countries. About 12 to 15% run an honest hybrid. About 45 to 50% are partner-served only, with no owned entities anywhere. The numbers, the methodology, the one honest caveat, and what they mean for buyers.

.png)

The numbers, up front

A few days ago I wrote that the country count on EOR homepages is the most misleading number in global employment, and I promised to come back with hard numbers on how the market actually splits. Here they are.

Of the EOR providers I audited where the structure was verifiable, about 40% claim and substantiate owned entities across most of their marketed countries. About 12 to 15% run an honest hybrid: real owned entities in some markets, openly disclosed partners in others. About 45 to 50% are partner-served only, with no owned entities I could verify anywhere.

The 45 to 50% number was the one that surprised me. Going in, I expected partner-served-only providers to be a meaningful slice. I didn't expect them to be roughly half.

The rest of this post is how I drew the lines, the one honest caveat, and what the numbers mean for buyers.

How I drew the lines

The universe was providers I audited where the structure could be verified from public disclosures, regulatory filings, or direct documentation. If I couldn't confirm the structure either way, I excluded the provider from the count rather than guess.

"Owned" required real owned entities across more than half of the provider's marketed countries. A genuine majority, not one or two flagship markets while the rest was outsourced.

"Hybrid" meant real owned entities somewhere, with the rest openly served by named, disclosed partners. The honesty of the disclosure mattered as much as the structure itself.

"Partner-served only" meant no owned entities verified anywhere, and reliance on third-party local firms for the employment relationship.

The "more than half of marketed countries" threshold for owned matters here. A provider that owns three countries while marketing 180 isn't operating an owned model in any meaningful sense. They're operating a partner model with a few flagship exceptions, and grouping them with full owned operators would have flattered the marketing rather than described the reality.

What "owned entity" actually means

I was strict about what counted as owned, because the word gets used loosely in marketing.

An owned entity is a legal company registered in the country, with operational substance: real staff, local payroll execution, direct relationships with the tax authority. It's not a holding-company shell, a sub-license of another global brand, or a registered presence that outsources the actual employment work to a local firm.

Even with that strictness, I gave providers the benefit of the doubt where the filings looked plausible. The point wasn't to disqualify anyone but to see, on consistent criteria, how the market actually splits.

One honest caveat

These numbers come from auditing claims and public disclosures, not from walking every registry in every country. If a provider claims to own an entity in a specific market and the structure is consistent with public filings and direct documentation, I counted it. I did not personally verify every single registration in every jurisdiction. That makes the numbers directional, not regulatory-grade, and the absolute shares are plus or minus a few points either way. The methodology is consistent across providers and the relative ordering is reliable. If anything, the "owned" share is slightly inflated, because some providers package licensed-local-specialist arrangements as "owned" in their marketing even where the operational reality is closer to hybrid.

Why the numbers matter for buyers

The 45 to 50% partner-served number is the one to sit with.

It means roughly half of the providers buyers consider in a typical shortlist don't actually own entities anywhere. They sell access to local firms. The local firm carries the employment relationship, the provider carries the contract with you, and the layer in between adds margin, complexity, and sometimes accountability gaps.

This isn't disqualifying on its own. A genuinely deep local partner can serve a specific country better than a global brand operating a thin owned entity there. The model can work.

What's disqualifying is when the structure is hidden. Providers that operate a partner-only model while marketing themselves as if they ran owned coverage are misrepresenting the product. The 12 to 15% running honest hybrids, with the structure disclosed clearly per country, are arguably the highest-integrity group in the category, even though they're the smallest.

And inside any one country, the share of providers who actually own there is much smaller than the headline. A provider in the owned group across 25 countries can still be partner-served in the 26th, which might be the country you care about.

How this connects to depth

The previous post made the case that depth in your countries matters more than breadth across the homepage. These numbers explain why the breadth claim is unreliable in the first place.

About half of the providers using "150+ countries" or similar language are doing so on the back of partner relationships rather than direct operation. The number is real in a contractual sense: they can probably arrange employment in those countries. It's misleading in a structural sense: they don't run those countries themselves.

That's why the right buyer move is country-by-country, not provider-by-provider. The same provider can be a tier-one option in one of your countries and a tier-three option in another.

What to do with this

A short list.

Don't disqualify partner-served providers automatically. Some are excellent in specific countries where the partner is genuinely deep and the disclosure is clean.

Do disqualify any provider that won't tell you, in writing, which structure they run in each of your target countries. The structural question has a right answer in every market, and providers who won't share theirs are signaling something.

Treat the honest hybrids as the undervalued option in the category. The 12 to 15% who tell you clearly which countries they own and which they don't are doing the procurement work for you.

When you ask, ask country by country. The provider-level summary obscures the country-level reality.

The takeaway

About half the providers in any given EOR shortlist don't own anything. About 40% own something real, though usually less than their marketing implies. About 15% run an honest mix and tell you which is which.

The model the provider runs matters. The honesty of the disclosure matters more.

I'll keep refining the working file as I add more providers to the audit. The numbers will move a few points over time, but the shape of the market won't.

I run Compareor, an independent comparator for EOR providers. If you want a read on which providers sit in which group for your specific countries, that's what we're for.

Get your shortlist

Takes ~3 minutes. No account needed.

June 3, 2026

6 min read

Every EOR contract has an expiration date

The EOR model has a built-in expiration date, somewhere between 15 and 20 employees in one country. Past that threshold, the EOR stops being the cheapest option and starts being a tax on growth. Most companies miss it for a year or more, because the contract doesn't mention it and nobody inside is responsible for noticing.

May 25, 2026

5 min read

Why "150+ countries" is the most misleading number in global employment

Every EOR homepage leads with a country count, and after auditing 150+ providers it's the number most likely to lead you to the wrong choice. Coverage comes in three forms, and depth in your countries matters more than breadth across 185 of them.

May 14, 2026

13 min read

FX Markup: The EOR Fee No One Discloses on Sales Calls

Of the seven cost layers in a typical EOR contract, FX markup is the most opaque — and on a 20-employee team, it costs more per year than the negotiated service-fee discount. Provider benchmarks from Deel (0%) to legacy providers (5%+), plus the contract redline that locks the spread.

Stay Updated on Global Hiring

Get weekly insights on EOR trends, compliance updates, and cost-saving strategies

Find a better EOR — without risk

Compare EOR providers to gain insights on cost, coverage, and contract flexibility, ensuring compliance and payroll continuity.

.png)

.png)