Deel Acquires Sastrify: What It Means for SaaS Spend and IT Management in 2026

Deel has acquired Sastrify, the AI-powered SaaS procurement platform, to unify hardware provisioning, software management, and spend optimization under Deel IT. Here's what this means for global teams.

.png)

Deel just acquired Sastrify, and the IT vendor stack just got shorter

On 5 May 2026, Deel — last valued at $17.3 billion with reported annualised revenue around $1.4 billion as of Q1 — announced the acquisition of Sastrify, the AI-driven SaaS procurement and management platform founded in Cologne in 2020. Deal terms were not disclosed. The Sastrify product, brand, and team are folding into Deel IT, and the combined offering ships this quarter under a single Deel IT label.

For Deel, Sastrify is the 10th acquisition since 2022 and the most strategically explicit move yet to expand beyond hardware-plus-payroll into software lifecycle management. For Sastrify, it is an exit at the top of a $45.3 million funding stack from HV Capital, FirstMark, Endeit Capital, Reimann Investors and others. For buyers of either platform, it changes the procurement equation in a way that matters: Deel IT now does what three separate categories of vendor — device management, SaaS management, and finance/spend tooling — used to do, and Sastrify as a standalone purchase is off the table.

This post covers what Sastrify actually does, what Deel IT looked like before and after, why Deel bought rather than built, what changes in the day-to-day IT and finance workflow, and the practical buying decision for companies on either side of the deal. If you are evaluating Deel as your employment platform independently, pair this with our Deel review and the EOR G2 leaderboard.

What is Sastrify?

Sastrify is a SaaS procurement and management platform — the operational layer that sits between a company's IT estate and the dozens or hundreds of software contracts it accumulates over time. Founded in 2020 in Cologne by Sven Lackinger (CEO) and Maximilian Messing (CTO), the company built a six-round funding stack of $45.3 million from HV Capital, FirstMark Capital, Endeit Capital (which led the $32 million Series B), Simon Capital, Reimann Investors, and TriplePoint Capital. By 2024 it was reporting roughly $31 million in revenue across approximately 70 mid-market and enterprise customers, primarily concentrated in DACH, the UK, and the US.

The product covers four core surfaces. The first is discovery — Sastrify connects to SSO, finance systems, and direct integrations with major SaaS vendors, then automatically maps every tool in use, who owns it, who actually uses it, what it costs, and when it renews. Most enterprises discover 30–40% more SaaS in their estate than IT had on file before running discovery, which is the immediate ROI that gets the platform deployed. The second surface is benchmarking — every contract is priced against $6 billion+ of live SaaS pricing data, which is the single hardest-to-replicate asset Sastrify owns. Buyers see whether they are paying above market for Salesforce, HubSpot, Snowflake, GitHub, Atlassian, or anything else with enterprise pricing. The third surface is procurement — automated renewal alerts, approval workflows, vendor negotiations, and intake forms tied directly to ownership and budget. The fourth is compliance — auto-generated vendor compliance documentation, SOC 2 / ISO certificate tracking, and audit-ready reports for DORA, NIS2, and the EU AI Act.

The combined effect is that Sastrify turns SaaS management from a quarterly spreadsheet exercise into a continuous, action-oriented workflow. Customers typically report 15–25% reduction in SaaS spend in year one, driven equally by cancelled shelfware (licences nobody uses), right-sized seats (paying for 200 seats when 140 are active), and renegotiated renewals where the benchmark data gives the procurement team leverage they did not have before.

What Deel IT looked like before — and what it looks like now

Before the acquisition, Deel IT was Deel's hardware-and-device offering: device procurement and provisioning across 130+ countries, mobile device management (MDM) on Windows / macOS / Linux / iOS / Android, device lifecycle management (storage, repair, retrieval, disposal), and IT support tickets. It plugged into Deel's HRIS so a new hire on Deel triggered a laptop order, an SSO provision, and a security policy push from a single onboarding event. It did not, however, do anything about software spend — SaaS contracts, licence allocation, renewals, benchmarks. That whole layer lived elsewhere, typically in finance spreadsheets, a separate SaaS management platform, or both.

After the acquisition, Deel IT's surface area expands to cover the whole IT lifecycle in a single platform: hardware provisioning, MDM, software procurement, licence assignment and right-sizing, renewal management, spend benchmarking, and compliance reporting. The integration the announcement emphasises is the joiner-mover-leaver flow — when an HR event happens in Deel's HRIS, the platform now provisions and deprovisions both hardware and software in one motion. New hire on Tuesday: laptop ships, MDM enrolls, Slack / Notion / GitHub / Salesforce seats assigned automatically based on role. Termination on Friday: laptop retrieved, SSO revoked, all SaaS seats reclaimed and the company stops paying for them on the next billing cycle. That is the unification thesis.

Why Deel bought rather than built

Building a SaaS management platform from scratch takes 18–24 months and produces the easy 60% — discovery, basic spend tracking, renewal calendars. The hard 40% — the pricing benchmark database, the negotiation playbooks, the vendor relationships needed to make procurement automation actually work — takes another 3–4 years and is mostly a function of accumulated transactional data. Sastrify's $6 billion+ benchmark dataset is the asset that nobody can replicate quickly, and it is the reason this acquisition makes sense at any plausible price.

It also fits Deel's M&A pattern. Since 2022, Deel has completed 10 acquisitions across payroll (PayGroup, PaySpace, Safeguard's payroll division), compensation (Assemble), payments (Atlantic Money), and IT (now Sastrify). The company has reportedly allocated $200–500 million for M&A in 2025 and is preparing for an IPO described as imminent for several quarters. The strategic logic — fill platform gaps before going public, present a single workforce-operating-system narrative rather than a payroll-with-add-ons narrative — is consistent across every deal.

What the deal likely cost

Deal terms were not disclosed, but the bounds are inferable. Sastrify raised $45.3 million across rounds, hit roughly $31 million revenue in 2024, and was likely growing 60–80% annually given the category and customer profile. SaaS management platforms have traded in 2024–2025 at 4–8× revenue for software-with-data-moat businesses; assuming Sastrify reached $50–60 million in revenue at the time of the deal and was sold at the higher end of that range given the strategic premium, the deal is probably in the $250–450 million range. That fits comfortably inside Deel's stated 2025 M&A budget and aligns with comparable transactions in the SaaS management space.

The SaaS spend problem the deal targets

SaaS now accounts for approximately 70% of total enterprise software budgets, up from 55% in 2020. The category is not slowing — the global SaaS management market alone is projected to grow from $4.58 billion in 2025 to $9.37 billion by 2030 at a 15.4% CAGR, and that is the management layer alone, not the underlying software spend. Total enterprise SaaS spending is in the hundreds of billions of dollars and rising, with AI-native tools (Cursor, Copilot, Glean, Anthropic, OpenAI) added on top of an already-bloated SaaS estate that the average mid-market company has not seriously rationalised in 5+ years.

The structural problem is that SaaS is purchased by every team, billed monthly or annually on dozens of corporate cards, renewed on auto-renew clauses that sometimes nobody remembers signing, and used (or not used) by individuals whose departures often do not trigger licence reclamation. The most common findings when a company runs SaaS discovery for the first time:

- 15–30% of licences are dormant — paid for, never logged in to in the last 90 days

- 10–20% of contracts are above market price by 15%+ (the benchmark gap)

- Multiple parallel subscriptions to the same category (three project-management tools, two diagramming tools, four note-taking apps)

- Renewal dates known to nobody, with auto-renew triggered before negotiation

- Off-boarded employees still on licence rolls 6–12 months after departure

Each of these is recoverable spend. Sastrify customer data suggests aggregate first-year savings of 15–25% of the SaaS bill, and that is the value proposition that justifies the management-layer subscription cost. For a company spending $5 million annually on SaaS — typical for a 500-person tech-leaning organisation — that is $750,000–$1.25 million in annual savings, which dwarfs the cost of either Deel IT or any standalone SaaS management platform.

How Deel IT + Sastrify works end-to-end

Day one after deployment, the platform connects to SSO (Okta, Azure AD, Google Workspace), HRIS (Deel's, or third-party via integration), and finance (NetSuite, Sage Intacct, QuickBooks). It crawls the SaaS estate and produces an inventory in 24–48 hours: every tool in use, every contract value, every renewal date, every owner, every active user. Where Deel IT is also handling devices and HR, the platform is doing a single sweep across the whole IT estate, not a fragmented discovery per category.

From there, the workflow runs continuously. New software requests come through an intake form tied to manager approval and budget owner. Renewal alerts fire 60–90 days out with a benchmark report attached, the procurement team renegotiates with leverage, and the renewal closes with the right seat count. Joiner events trigger automatic licence assignment based on role; leaver events trigger automatic reclamation. The compliance layer auto-attaches the vendor's latest SOC 2 / ISO 27001 / data processing agreement to the contract record, which is the difference between a 2-week DORA / NIS2 audit and a 2-day one.

The unique advantage of running this inside Deel IT is the HR-data integration. Most SaaS management platforms know who you are paying for, but not who actually works at the company today, who changed roles last week, or who is leaving in two weeks. Deel IT does. That is the integration thesis the deal rests on.

The competitive landscape after this deal

Sastrify was one of three or four serious SaaS management platforms with a defensible benchmark dataset. The remaining standalone vendors are Zylo, Productiv, Torii, BetterCloud, and Vertice — each with somewhat different positioning.

PlatformPositioningBenchmark depthBest forDeel IT (Sastrify)Bundled with HRIS, devices, payroll$6B+ pricing dataCompanies on DeelZyloEnterprise standalone$34B+ data (largest)Enterprise (1,000+ employees)ProductivUsage-analytics-firstLimited benchmarksMid-market with usage focusToriiNo-code automation focusLimited benchmarksSMB to mid-marketBetterCloudSaaS ops + automationLimited benchmarksIT operations heavyVerticeNegotiation-as-a-serviceStrong benchmarksOutsourced negotiation focus

The category is not consolidating away — it is bifurcating. One group of buyers will continue choosing standalone, best-of-breed SaaS management because they want the deepest benchmark database (Zylo) or the strongest negotiation service (Vertice). The other group — and this is where the Deel acquisition matters — will collapse the category into the workforce platform they already use, giving up some specialisation in exchange for one vendor, one billing relationship, one integration to maintain. Deel is betting the second group is bigger.

What this means if you are already on Deel

If you are already a Deel customer for EOR, payroll, contractor management, or HRIS — and especially if you are on Deel IT for hardware — Sastrify becomes a value-add bundled into the platform rather than a separate procurement decision. Pricing will be announced this quarter; expect a tiered model where SaaS management is included in higher-tier Deel IT contracts and available as an add-on at lower tiers.

The practical advice is to wait until pricing publishes, then run the maths against your current SaaS management cost. If you are not running a SaaS management platform today, the bundled offering is almost certainly worth it — even partial visibility into 50–60 SaaS contracts will save more than the bundle costs. If you already run Zylo or Productiv on a long-term contract, the switching decision depends on contract end date and how deep you are into the existing platform's data history.

What this means if you are not on Deel

If you do not use Deel for employment, the acquisition does not directly affect you — except that Sastrify, as a buying option, has now exited the standalone market. Existing Sastrify customers retain the product, but new buyers cannot purchase Sastrify without entering the Deel ecosystem. For most non-Deel companies the procurement choice now narrows to Zylo, Productiv, Torii, BetterCloud, or Vertice depending on size and need.

For non-Deel companies who are simultaneously evaluating an EOR or global payroll provider, the acquisition adds a new variable. Bundling SaaS management with employment infrastructure is genuinely useful if the employment volume justifies Deel pricing, but Deel is not the cheapest EOR — it sits in the premium tier. Compare alternatives using our comparison tool and check the G2-ranked EOR leaderboard before treating the bundled SaaS layer as a tiebreaker.

Frequently asked questions

When does the combined Deel IT + Sastrify offering go live?

Q2 2026, per the acquisition announcement. Existing Sastrify customers continue using the standalone product during the transition. New customers buying SaaS management capabilities from Deel will be onboarded into the integrated platform from this quarter forward.

Was the deal price disclosed?

No. Sastrify raised $45.3 million across six rounds, hit ~$31 million revenue in 2024, and was likely sold at a 4–8× revenue multiple typical of SaaS-management category transactions, putting the implied range somewhere between $250–450 million. Neither company has confirmed.

Does this affect Deel's EOR or payroll pricing?

Not directly. Deel IT is a separate product line from Deel's EOR and payroll services, and pricing for those services has not changed as a result of the acquisition. Our Deel review covers current EOR and payroll pricing in detail.

What happens to Sastrify customers who are not on Deel?

Existing Sastrify customers retain access to the product at current contract terms. Renewals will likely move them onto the Deel IT platform branding, with the underlying capabilities maintained. The Sastrify product is not being sunset.

Does the Sastrify benchmark database remain proprietary to Deel?

Yes. The $6 billion+ pricing benchmark dataset moves with the team to Deel and remains the differentiating asset behind the Deel IT software-management offering. It is not being licensed externally to competing platforms.

Are there alternatives if I do not want to consolidate around Deel?

Yes. Standalone SaaS management options remain in market: Zylo (largest benchmark database), Productiv (usage-analytics focus), Torii (no-code automation), BetterCloud (SaaS ops), and Vertice (negotiation-as-a-service). Each is a defensible buy depending on company size and priorities.

How does this affect Deel's IPO timing?

Deel has been preparing for an IPO reportedly targeted for 2026. The Sastrify acquisition is consistent with a pattern of pre-IPO platform-completion deals — broaden the product story, justify a higher revenue multiple, and present a workforce-operating-system narrative rather than a payroll-with-add-ons narrative. It does not change the IPO timeline materially but it strengthens the platform pitch.

Bottom line

The Sastrify acquisition is the strongest signal yet that Deel intends to be the workforce operating system rather than a payroll provider with adjacent products. Adding SaaS management to a platform that already covers EOR, contractor management, payroll, HRIS, and device management completes a real story — onboarding-to-offboarding for both people and the tools they use, in a single billing relationship with a single integration footprint. The strategic logic is sound.

The execution risk is real. Sastrify's value lives in the depth of the benchmark database and the procurement workflows, both of which require careful preservation through integration. The next two quarters — and specifically how cleanly the joiner-mover-leaver flow connects HR events to licence assignment — will determine whether the bundle delivers on the unification thesis or remains two products under one logo.

For buyers, the practical decision is unchanged in shape but slightly different in input. If you are on Deel, the bundled Deel IT + Sastrify offering is likely the most cost-effective SaaS management option available to you this quarter, and the right move is to wait for pricing and run the maths. If you are not on Deel, the SaaS management category just lost one competitor but the remaining choices (Zylo, Productiv, Torii, BetterCloud, Vertice) are still plenty deep — Sastrify-as-a-standalone is gone, but the alternatives are not. And if you are simultaneously deciding on EOR and SaaS management, the Deel bundle adds a real variable to the procurement decision, but it is not a tiebreaker on its own — the underlying employment platform still has to be the right fit. Compare the EOR leaderboard and read the Deel review before letting the IT bundle drive the decision.

Get your shortlist

Takes ~3 minutes. No account needed.

June 3, 2026

6 min read

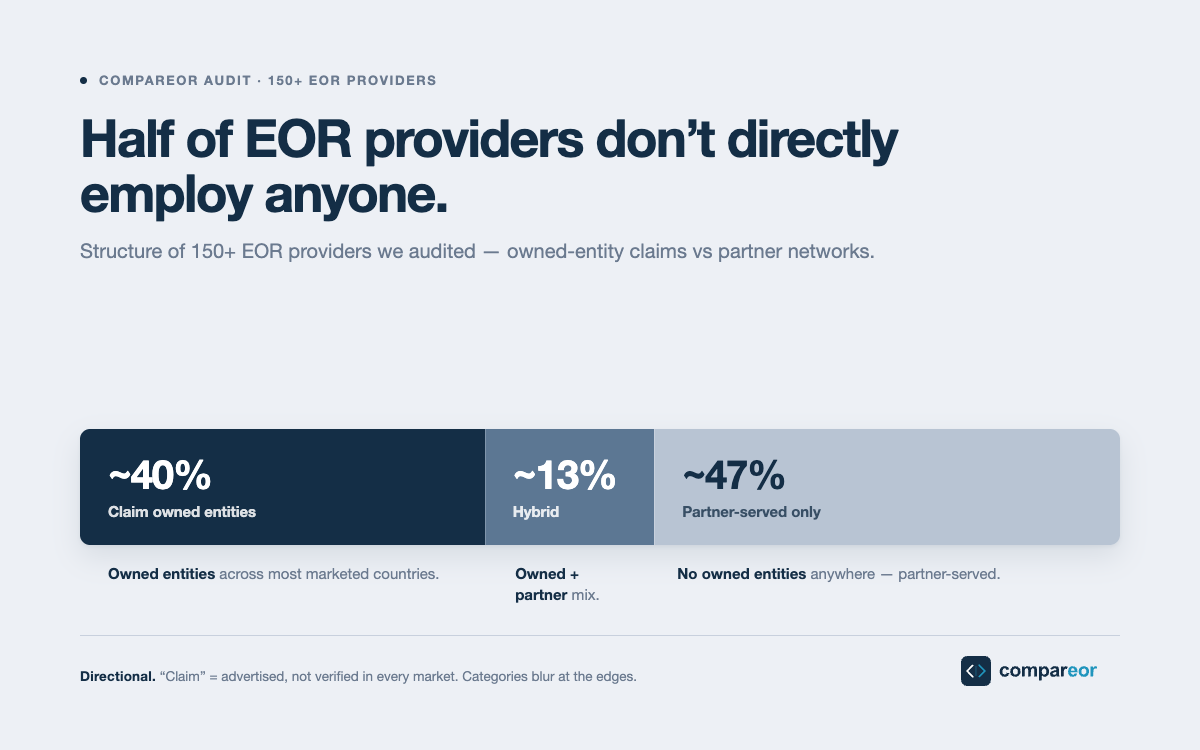

I checked the structure of 150+ EOR providers. Here's how many actually own their entities.

About 40% of EOR providers I audited claim and substantiate owned entities across most of their marketed countries. About 12 to 15% run an honest hybrid. About 45 to 50% are partner-served only, with no owned entities anywhere. The numbers, the methodology, the one honest caveat, and what they mean for buyers.

June 3, 2026

6 min read

Every EOR contract has an expiration date

The EOR model has a built-in expiration date, somewhere between 15 and 20 employees in one country. Past that threshold, the EOR stops being the cheapest option and starts being a tax on growth. Most companies miss it for a year or more, because the contract doesn't mention it and nobody inside is responsible for noticing.

May 25, 2026

5 min read

Why "150+ countries" is the most misleading number in global employment

Every EOR homepage leads with a country count, and after auditing 150+ providers it's the number most likely to lead you to the wrong choice. Coverage comes in three forms, and depth in your countries matters more than breadth across 185 of them.

Stay Updated on Global Hiring

Get weekly insights on EOR trends, compliance updates, and cost-saving strategies

Find a better EOR — without risk

Compare EOR providers to gain insights on cost, coverage, and contract flexibility, ensuring compliance and payroll continuity.

.png)

.png)